Retirement is supposed to be the reward for years of hard work — a time to relax, travel, and enjoy life. But for many, it also becomes a minefield of sales pitches. Suddenly, your inbox is flooded with offers for "protection plans," "guaranteed income," and "peace of mind" — all designed to make you feel like you’re missing out if you don’t buy in.

The truth? Many of these so-called “retirement essentials” are not only unnecessary — they can quietly drain your savings over time. Here are eight common retirement purchases that you may want to reconsider.

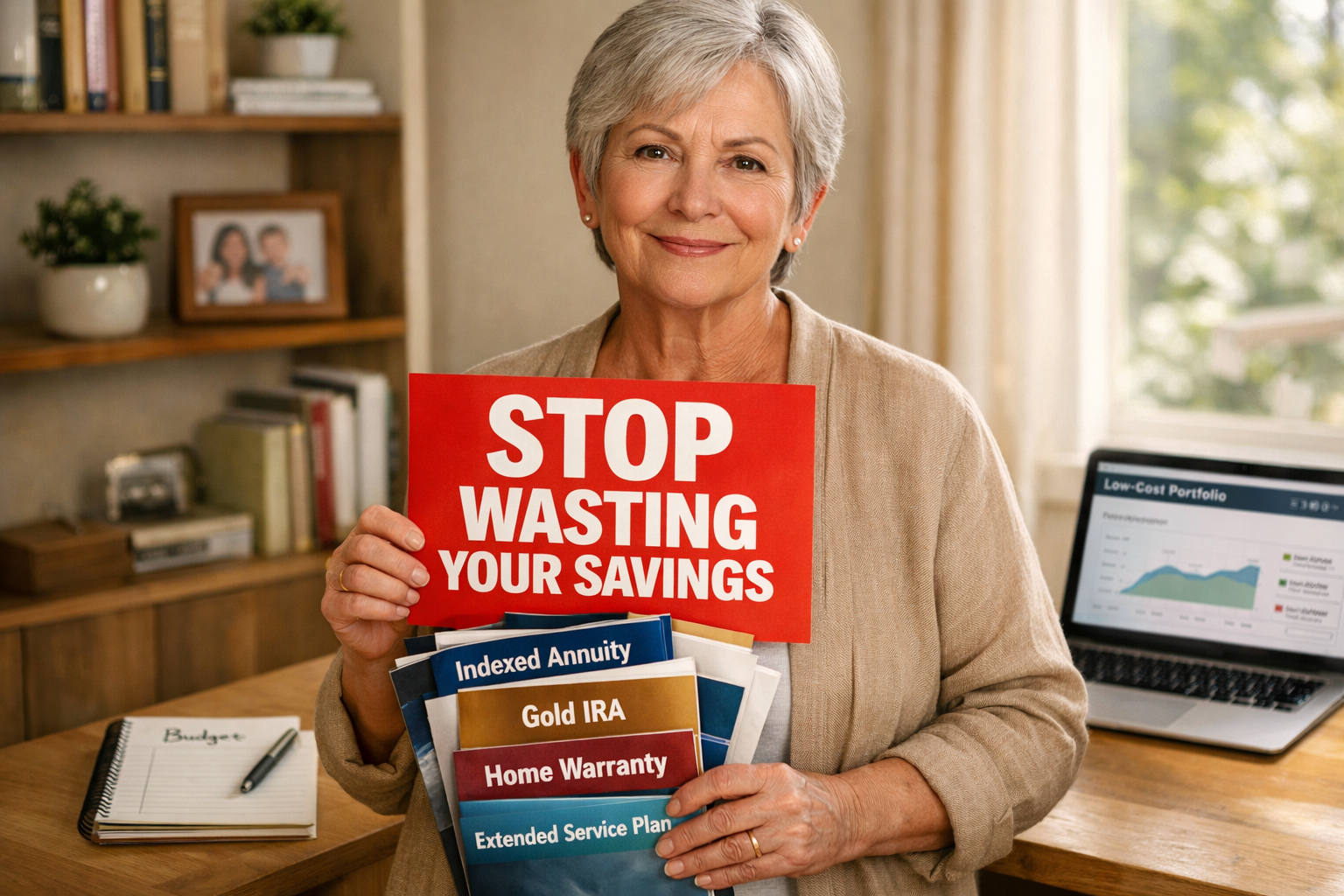

1. Home Warranty Plans: A “Safety Net” That Costs More Than It’s Worth

You’ve probably heard the pitch: “What if your air conditioner breaks down? Your homeowner’s insurance won’t cover it.” That’s why companies like Choice Home Warranty sell home warranties — promising to cover repairs for appliances, plumbing, and electrical systems.

But here’s the catch: most of these plans come with high monthly fees, deductibles, and exclusions. For example, if your furnace is 10 years old, the warranty may not cover it — even if it fails. And if you’ve already paid for a home warranty, you might find that the cost of a single repair is less than your monthly premium.

In reality, most retirees are better off setting aside a small emergency fund for home repairs. A $500–$1,000 rainy-day account can cover unexpected issues without the long-term cost of a warranty.

2. Whole Life and Cash-Value Life Insurance: Not the Retirement Investment You Think

Life insurance is meant to protect dependents — not to be a retirement investment. Yet many retirees are sold whole life policies as “tax-advantaged” or “estate planning tools.” The reality? These policies come with high premiums, modest returns, and complex rules.

For example, a $100,000 policy might cost $10,000 per year in premiums. That’s money you could have invested in a low-cost index fund — where it could grow over time. Instead, you’re locking in a slow, low-yield return with high fees.

If you’re already financially secure and your children are independent, that money is better spent on a diversified portfolio — not a policy that benefits the insurance company more than you.

3. Indexed Annuities: “Safe” Income With Hidden Costs

Indexed annuities are often marketed as “safe” retirement income. They promise upside potential with limited risk — but only if you read the fine print.

In reality, these products come with caps on returns, participation rates, surrender charges, and layered fees. For example, if the market goes up 10%, you might only get a 5% return — and that’s after fees. Plus, your money is locked in for years, making it hard to access if you need it.

Many financial planners and state regulators — including the Minnesota Attorney General — warn that indexed annuities are often unsuitable for seniors. Simpler, more transparent options like low-cost annuities or dividend-paying stocks can offer better results.

4. Gold IRAs and Precious Metal Accounts

Gold is often sold as a “safe haven” during economic uncertainty. But gold IRAs come with high setup fees, storage costs, and aggressive sales tactics. And unlike stocks or bonds, gold doesn’t generate income — it just sits there.

If you’re worried about inflation or market volatility, consider a small allocation to commodities — but not a large portion of your retirement portfolio. A better strategy is to diversify across assets that generate income, like dividend stocks or bonds.

5. Premium Identity Theft Monitoring

Identity theft is real — but many retirees already have free protections. Credit card issuers, banks, and even Medicare offer fraud alerts and monitoring. The Government Accountability Office (GAO) has found that paid monitoring services can’t prevent fraud — they only detect it after the fact.

And if a data breach happens, companies and government agencies often offer free identity protection going forward. Spending $100+ per year on a premium plan may not be worth it — especially when you can stay informed through free tools.

6. Extended Warranties and Service Plans

Retailers know that retirees value security — which is why extended warranties are heavily marketed to this group. But these plans are often overpriced and under-delivered.

For example, a $200 extended warranty on a TV may cost more than the repair would cost — and it may not cover the exact issue you have. Many major purchases already come with manufacturer warranties, which are often better than the extended version.

A better strategy? Keep a small emergency fund for repairs — and only buy extended warranties on high-cost items you use frequently.

7. High-Fee Managed Investment Accounts

Many retirees are steered into actively managed portfolios with high annual fees — often over 1%. While these plans promise expert guidance, the fees can eat into your returns over time.

In contrast, low-cost, diversified strategies — like index funds or ETFs — can outperform high-fee managed accounts. And with today’s technology, you can manage your own portfolio through simple, affordable platforms.

8. Lifestyle Subscriptions: Convenience at a Cost

Meal kits, lawn care, concierge services, and travel clubs are often sold as “retirement conveniences.” But if you’re already retired, you may have more time — and less need — for these services.

Paying $100 per month for a meal kit or lawn service may seem small — but over 20 years, that’s $24,000. And if you can do these tasks yourself, you’re better off keeping that money in your pocket.

The Bottom Line

Retirement shouldn’t be about buying more products — it should be about making smarter decisions. Many of the tools sold to seniors are designed to generate profit for the seller, not protect your financial future.

Before you sign up for any new product, ask yourself:

- Does this truly improve my financial security?

- Are there cheaper or simpler alternatives?

- Am I making this purchase out of fear or genuine need?

If the answer is no, it’s time to walk away.

This blog post was written based on information from FinanceBuzz and consumer protection resources. For more on retirement planning and avoiding financial pitfalls, visit the Bureau of Consumer Protection.

The truth is, the financial industry has spent decades marketing to seniors — not because they care about your peace of mind, but because retirees represent a massive pool of accumulated wealth. And where there’s money, there are salespeople ready to offer “solutions” — even if those solutions don’t actually solve anything.

But here’s the empowering part: you don’t need to buy into the hype.

Retirement is not about accumulating more stuff — it’s about preserving your freedom. That means saying “no” to products that promise security but deliver complexity, fees, and hidden costs. It means choosing simplicity over sales pitches. And it means trusting yourself — or a trusted advisor — to make decisions that align with your real needs, not someone else’s profit margin.

Start by reviewing your current expenses. Are you paying for a home warranty you rarely use? A gold IRA that’s underperforming? A subscription service you forgot you signed up for? Cancel what you don’t need — and redirect that money into a low-cost, diversified portfolio or a simple emergency fund.

And if you’re unsure whether a product is right for you, ask yourself this:

“Would I still buy this if I knew the salesperson earned a commission from it?”

If the answer is no — you’ve got your answer.

Final Thought: Your Retirement, Your Rules

You worked hard to get here. Don’t let fear, guilt, or aggressive marketing convince you that you need to spend your hard-earned savings on products that don’t serve you.

The best retirement plan isn’t the most expensive one — it’s the one that’s clear, affordable, and aligned with your goals. Whether that means managing your own investments, using free identity protection tools, or skipping the extended warranty on your new refrigerator — you’ve got the power to choose.

And if you’re ever unsure? Talk to a fiduciary advisor — someone legally required to act in your best interest — not a salesperson.

Because retirement isn’t about buying more. It’s about living better — with less stress, less clutter, and more control.

This blog post was written based on consumer insights from FinanceBuzz and the Bureau of Consumer Protection. For more on avoiding retirement scams and making smart financial decisions, visit your state’s consumer protection office or the FTC’s website.

Share:

Tax Refunds in 2026: Why Millions of Americans Are Counting on Them More Than Ever

Tax Justice Isn’t Just About Money — It’s About Women Holding Up Broken Systems